I heard about a great success story during my research about business development companies (BDCs).

The story involves billions of pounds of ice, millions of dollars of loans, and a company growing like crazy thanks to a middle-market lender.

In an unlikely twist, the lender then gained control – even though the company was healthy – in a friendly buyout.

They invested more money and finally sold the company for a huge profit. It was the single largest and most successful deal in the lender’s history.

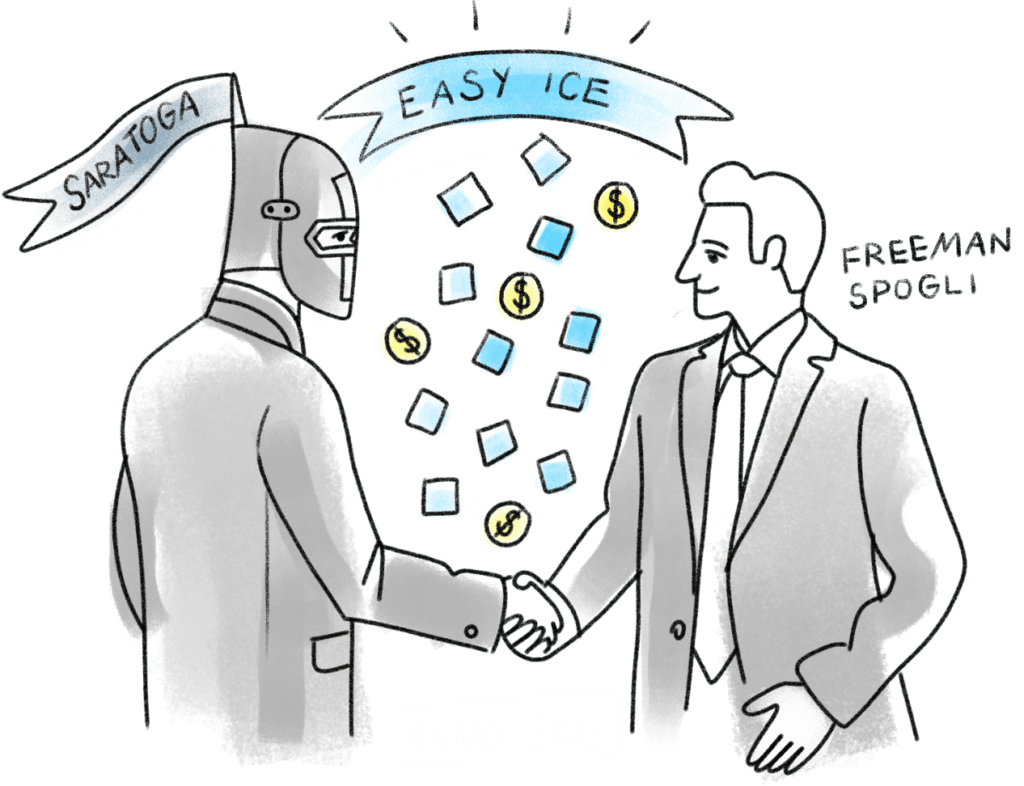

This is the story of Easy Ice and Saratoga Investment Corp.

Introduction

There are two main subjects in this story: Easy Ice, a subscription-based commercial ice machine business, and Saratoga Investment Corp, a lender of money to growing companies.

Let’s start with Easy Ice.

History of Easy Ice

In 2009, Mark Hangen and John Mahlmeister founded Easy Ice.

They planned to offer a subscription-based business model that “takes the hassle out of owning a commercial ice machine.”

Ice machines are known for having high maintenance costs and often needing expensive repairs.

Hangen and Mahlmeister believed that a subscription-based model for ice machines could be a big business.

This same monthly subscription model was already being used for commercial dishwasher machines in the food service industry, racking up tens of millions of dollars for companies like EcoLab and Auto-Chlor.

Monthly Ice Machine Rentals

Here’s how the Easy Ice business model works:

Hotels and other businesses can either buy and manage a huge ice machine, typically for $3,200, like this one:

Or business owners can just pay a monthly fee to Easy Ice to rent it.

The monthly subscription fee includes leasing the ice machine plus all service and maintenance costs.

The rental model distinguishes Easy Ice from competitors who only sell the machines outright, often for thousands of dollars. Renting from Easy Ice reduces overall costs for the business owner.

By January 2020, Easy Ice had rented over 25,000 ice machines in the USA.

That’s a lot of ice machines.

Growth of Easy Ice

Ice machine rental was an entirely new category of business.

In order to grow, Easy Ice needed a lot of money to buy thousands of ice machines which they would then rent out.

Easy Ice also wanted more sales territory and more market share. But they needed more money to expand.

Most traditional banks wouldn’t lend money to Easy Ice in 2013. It was still too new of a business. Perhaps it was also too risky to secure a business loan with high-maintenance ice machines that would be scattered across the country.

That’s where Saratoga Investment Corp comes in.

Mister Moneybags Comes to Town

Easy Ice wouldn’t qualify for a large bank loan, and they were too small to issue a bond.

So how could they get money to grow?

Enter business development companies, also known as BDCs.

BDCs make multi-million dollar loans to companies that need money to grow and don’t qualify for traditional lending options.

There are fifty publicly-traded BDCs. Together they represent around $100 billion dollars of funding and market capitalization.

I’ve written more about BDCs on my research article here, including the most popular ones like Ares and research resources like the BDC Reporter.

Taking a BDC loan was the best choice for Easy Ice. They could borrow lots of money without giving up ownership, or equity, like a venture capital or private equity firm might require. Taking a BDC loan would also make it easier for Easy Ice to have flexible repayment terms, like Payment In Kind (PIK).

Fun fact: A PIK loan allows a company to make their interest payments later in time. It means you’re paying your old debt with new debt, and that can be seen as risky.

The BDC that Easy Ice selected was Saratoga Investment Corp. Here’s what Mark Hangen, the Easy Ice CEO, said at the time:

“When evaluating options, a CEO needs to think beyond just the bottom-line cost of capital. For us, the right lending partner was a BDC because Saratoga… recognized that my business was best served by reinvesting my free cash flow to grow.”

A Cash Infusion

Easy Ice raised $20,000,000 in a deal that was announced on January 28, 2014.

This included money from two sources:

- $12,000,000 as a first-lien loan from Saratoga Investment Corp., a BDC that specializes in making customized loans for mid-sized companies.

- Plus $8,000,000 from private investors.

Let the Good Times Roll

Flush with their $20 million of new capital, Easy Ice entered new markets, acquired competitors, hired more staff, and increased their market share.

The $12 million investment from Saratoga helped Easy Ice grow its customer base by 181%. (source) They built a presence in 45 U.S. states and tripled their revenue and earnings.

Customers loved the ice machine rental strategy.

Costly Growth

Easy Ice’s master growth plan was working, but it was expensive.

For each new $179 monthly client, they needed at least $3,000 in immediate capital to buy the ice machine, plus thousands of dollars in labor costs for sales and support.

According to annual reports from Saratoga, Easy Ice had an operational profit in both 2015 and 2016. But if you calculated the cost of interest on their loans, Easy Ice was showing a net loss.

This was not alarming to Saratoga. Since its inception, Easy Ice never had much free cash flow. They were always redeploying any profits back into the company.

Saratoga understood that management could always dial back their growth strategy and turn Easy Ice into a very profitable company.

Payment in Kind

The original lending agreement from Saratoga was structured to use Payment-in-Kind (PIK). Easy Ice wouldn’t have to make traditional interest payments on their loan until it was due in several years.

PIK loans are usually a worst-case scenario. A company is paying their debt with more debt. This can signal cash flow problems and a lack of profitability.

But Saratoga wasn’t worried. They had planned for this and they continued to see healthy market share increases as Easy Ice expanded. Profits would come later.

An Unexpected Change in Control

Saratoga loaned Easy Ice more money over eight additional funding rounds. These loans allowed Easy Ice to hire more staff and make a few strategic acquisitions. They also cemented Saratoga’s role as a trusted partner to Easy Ice.

In 2017, a surprising opportunity popped up.

Reddy Ice, a manufacturer of packaged ice and an early private investor in Easy Ice, was preparing to be sold to a private equity firm. They wanted to sell their 45% ownership stake in Easy Ice in order to streamline their balance sheet.

The price was $8 million, valuing Easy Ice – a money-losing, capital-intense, debt-burdened company – at $17.78 million.

Saratoga leapt at the opportunity. They knew that despite the net losses, there would someday be gold at the end of this chilly rainbow.

This purchase of such a large percentage of the company was extremely unusual.

Most lenders don’t take majority control of companies. If they do, it’s as a last resort and typically when a company is failing.

But Easy Ice was definitely not failing.

Saratoga knew they could make money as Easy Ice would continue to grow with their financing. They saw the potential and were willing to take the risk in buying the equity from their BDC funds.

Saratoga’s Transaction Details

Saratoga Investment Corp purchased 45% of Easy Ice in February 2017 from Reddy Ice. This made them the largest shareholder and gave them control of the company.

At the same time, Saratoga dramatically increased their loan to Easy Ice from $13.8 million to $26.7 million. This additional funding would allow Easy Ice to acquire a competitor in Chicago.

Saratoga also invested in an $8 million preferred-equity position, buying out 45% of the company equity from Reddy Ice.

Sale of Easy Ice

By 2018, Saratoga was already seeing results at Easy Ice. They quietly marked up the value of their $8 million preferred equity position by $2 million in their annual report.

And then suddenly, without any warning: they sold everything.

Saratoga announced on December 31, 2019 that they had sold Easy Ice.

They sold it to Freeman Spogli & Co., a private equity firm which also owns El Pollo Loco and had previously invested in Mattress Giant, Advance Auto Parts, and Piggly Wiggly. (source)

Saratoga saw a cool $31.2 million profit on the sale of their Easy Ice investment.

It was the single largest deal in Saratoga’s history.

Conclusion

Business development companies like Saratoga are supposed to operate more like banks than venture capital firms. They operate with a much lower risk tolerance. BDCs rarely take control of the companies that they lend to, and never when things are going well.

This was a unique situation. The $31.2 million windfall happened because of a few critical factors:

- Easy Ice needed lots of money to grow.

- Saratoga lent Easy Ice money when nobody else would and with flexible repayment terms.

- A prior investor, Reddy Ice, needed to exit during an unprofitable time.

- Saratoga was willing to double-down on a business they had become familiar with.

In the end, Saratoga Investment Corp. made their largest ever debt investment, bought a controlling equity stake, and then sold their shares in Easy Ice for a very large profit.

Now that’s cold.

Ice cold!

Timeline

- 2008 – Easy Ice founded in Marquette, MI, USA.

- 2013 – Easy Ice begins seeking capital investors to fund its expansion efforts.

- 2014 – Easy Ice announces that it has raised $20m in funding. Saratoga invests $12m with the remainder from private investors.

- 2017 – Saratoga takes control of Easy Ice in February 2017 by investing $8 million in a preferred-equity position, buying out 45% of Easy Ice from Reddy Ice. Saratoga simultaneously increased their first lien investment by 93%, from $13.8 million to $26.7 million.

- 2017 – Saratoga completes a recapitalization of Easy Ice in October 2017 with the support of Madison Capital. Saratoga received repayment of $10.2 million of the Easy Ice debt and converted the rest ($16.5 million) to a second-lien position. Saratoga’s debt was now second in line for repayment, behind their new investor, Madison Capital.

- 2019 – Reddy Ice was sold to Stone Canyon, a company backed by Michael Milken.

- 2019 – Freeman Spogli & Co. acquires Easy Ice from Saratoga.

- 2020 – I researched and published this fantastic recap on my blog 😂. If you’re still reading, why not sign up for my informal and free Friends Newsletter? I share stuff like this every few weeks. Join 8,000 other CEOs, Founders, business nerds, and even art curators who love it. See why here.

Key players

- Mark Hangen and John Mahlmeister, co-founders of Easy Ice

- Christian L. Oberbeck, Chairman and CEO of Saratoga Investment Corp.

- Michael J. Grisius, President and Chief Investment Officer of Saratoga

- Joe Burkhart, Managing Director and Head of Business Development of Saratoga

- Charles Phillips, Managing Director of Saratoga

- John Hwang, Partner at Freeman Spogli

Saratoga Investment Corp

Saratoga is a BDC based in New York City that offers capital and guidance to middle-market businesses. In plain English, that means they:

- Are more comfortable with risk than traditional banks

- Will fund new expansion projects

- Partner with existing leadership to create a business plan to ensure payback

Easy Ice

Easy Ice was founded in 2008 in Marquette, MI, USA. The company prides itself on knowing ice better than anyone. They even maintain a blog to educate subscribers about different aspects of ice. Easy Ice sells monthly subscriptions, which include a commercial ice machine along with all service and support. The subscriptions offer:

- Energy-efficient Hoshizaki or Manitowoc ice machines

- Lifetime guarantee

- Biannual preventative maintenance

- 24/7 customer support

Financial Terms of the Deal

Saratoga made a total investment of $40.4 million dollars in Easy Ice, including:

- A first lien loan with total interest of $3.3 million

- A second lien loan totalling $27.9 million

- Preferred equity totalling $10.7 million

After the new buyer repaid the debt, Saratoga received an additional $35.6 million in fees, interest, and proceeds. They saw a $31.2 million gain from their Easy Ice preferred equity investment with a cost of $10.7 million.

Additional Information

- Casey Alexander, a Compass Point analyst, believes that Easy Ice could have been a problematic investment for Saratoga. In April of 2020, during market uncertainty from coronavirus, Alexander wrote, “SAR dodged a potentially fatal bullet with the sale of Easy Ice, a provider of ice-making machines for hotels, restaurants and bars. Still, we understand that lower middle market borrowers are more vulnerable to business stoppages. Access to SARs untapped SBA debentures could be critical in offering additional capital to distressed portfolio companies, but the stresses from the current stoppage may be too much for some of them.”

- As part of the sale to Freeman Spogli, Easy Ice CEO Mark Hangen and COO John Mahlmeister agreed to remain with Easy Ice for a minimum of five years. In a 2020 interview, Hangen alluded to the fact that Easy Ice may be looking to acquire smaller competitors

Additional Sources

- Saratoga: “Led $26.7 million in unitranche and $8.0 million in preferred equity financing to support the management team’s purchase of the business from the parent company.”

- “Saratoga Investment Corp.’s objective is to create attractive risk-adjusted returns by generating current income and long-term capital appreciation from its debt and equity investments.” (Direct quote)

- Saratoga Investment Corp (SAR) Q4 2020 Earnings Call Transcript, where they discuss details of the Easy Ice sale and numbers

- Saratoga Investment Corp. Announces Recapitalization of Easy Ice Investment, an article discussing the strategic partnership between Saratoga and Easy Ice

- Easy Ice Raises $20 Million in Growth Financing, a more detailed accounting of the numbers involved and the future of the restructuring

- Saratoga Investment Corp. Announces Fiscal Third Quarter 2020 Financial Results and Quarterly Dividend of $0.56 per Share ($2.24 per Share on an Annualized Basis), a quarterly finance report listing the sale of Easy Ice to a different private equity firm

- Investment Profile: Easy Ice, a case study done of Easy Ice and Saratoga

- Unitranche Debt Definition, a detailed explanation of unitranche debt

- Easy Ice, LLC has been Acquired by Freeman Spogli & Co. and Management

- About BDCs from Saratoga Investment Corp

- Easy Ice: Bringing in BDC Financing Article explains why Easy Ice chose financing from the BDC versus other options.

- Saratoga Investment Corp. Announces Recapitalization of Easy Ice Investment

- Saratoga’s Case Study: Investment Profile on Easy Ice

- Easy Ice Raises $20 Million in Growth Financing (2014)

- Saratoga Investment Corp (SAR) Q4 2020 Earnings Call Transcript

- Quiznos, Iron Bay, Easy Ice, and the Redmen Local news article about Easy Ice sale.

Credits: Thanks to Bethany Mangle, Danielle Dahl, and more for research help. Thanks to Fru Pinter for graphics. Thanks to Claire Boston and Joe for editing suggestions.

Do you have any Easy Ice gossip or additional facts I can add to this story? Notice a correction that needs to be made? Send me an email or message me on Twitter.